How to Launch a Copy Trading Platform: The Broker’s Technical Guide

Most brokers that add copy trading treat it as a feature. The ones generating sustainable revenue from it treat it as a product line — and build accordingly.

The distinction is more than semantic. Copy trading infrastructure has a direct bearing on spread capture, fund manager acquisition, and follower retention. A platform that executes copy trades 200 milliseconds behind the signal provider’s entry does not just frustrate followers — it compresses the margin that makes the entire model viable and turns the brokerage’s highest-value client segment into a churn risk.

This guide is for brokerage operators who have decided to launch copy trading and want to do it correctly: with the right execution architecture, a defensible fee model, and risk controls built into the stack from day one.

The Financial Case for Getting This Right

A mid-size brokerage running 4,000 active retail traders generates approximately $180,000 per month in spread revenue at a 1.2-pip average effective spread across major FX pairs — an illustrative figure based on standard broker unit economics.

Add a copy trading layer with 800 followers replicating six fund managers, and the revenue picture changes materially.

Copy followers consistently trade at higher average lot sizes than solo retail clients — industry-reported benchmarks suggest 35–50% higher volume per active account. On an 800-follower base, that translates to an estimated $28,000–$34,000 in incremental spread revenue per month. Beyond spread, a broker retaining 20% of a fund manager’s standard 20% performance fee on $2M AUM generating 8% quarterly returns adds approximately $6,400 per quarter in platform revenue — from a single manager.

Retention economics compound this further. Platforms that have reported social trading data publicly — eToro being the most cited — consistently show copy participants depositing two to three times more than non-copy peers and churning at roughly half the rate. For a brokerage modelling LTV by segment, that difference is structural, not marginal.

The execution risk is equally real. When copy trades execute 180–250 milliseconds behind signal price — a common gap in plugin-based implementations — slippage on fast-moving signals erodes follower PnL, compresses visible fund manager performance metrics, and accelerates churn among the most profitable cohort on the platform.

Why Most Copy Trading Launches Underperform

The default brokerage approach is to integrate a third-party copy trading plugin onto an existing MT4/MT5 installation. That approach has a structural flaw: the copy execution layer sits outside the primary trade engine, creating a latency gap between signal generation and follower order submission.

Three failure points appear consistently across poorly architected implementations.

Signal lag. The bridge between the fund manager’s account and follower accounts adds milliseconds at every step. In a market that moves 15 pips in three seconds — not unusual around NFP, central bank decisions, or geopolitical breaks — a 200-millisecond lag translates to 1.0–1.5 pips of entry slippage per copied trade. For a follower targeting 10 pips, that is a 10–15% compression of trade merit on every replication.

Risk management blindness. Vanilla copy trading implementations do not give the risk desk visibility into aggregate exposure generated across follower accounts. When a popular fund manager enters a concentrated GBP/USD position and 600 followers replicate it within seconds, the brokerage is running material unhedged directional exposure that may not appear in any risk report. It is not a theoretical scenario — it is a structural gap in plugin-based architectures.

Fee model misalignment. Brokers that launch copy trading without modelling the three-way revenue structure — broker spread, fund manager performance fee, platform management fee — frequently find they have built a product that attracts fund managers without generating proportional brokerage revenue. The three streams are additive and need to be configured before launch, not retrofitted after the first fund manager complaint.

Reframing Copy Trading as a Margin Expansion Tool

Properly architected, copy trading generates compounding revenue across three simultaneous streams: spread capture from follower trading volume, a percentage share of fund manager performance fees, and reduced per-client acquisition cost as fund managers bring their own audiences to the platform.

Brokers running native copy trading infrastructure — integrated at the execution layer rather than appended via plugin — report two to three percentage points of additional net margin attributable to copy-related volume, relative to total platform revenue. The mechanism is straightforward: followers trade more, stay longer, and deposit more than the solo retail baseline.

The enabling architecture principle is sub-50-millisecond copy replication. That target is achievable with the right infrastructure. It is not achievable with a plugin sitting above the order management system.

Operator-Level Steps: How to Build It Right

Step 1 — Define the Copy Model Before Touching Technology

Choose between PAMM (Percent Allocation Management Module), MAMM (Multi-Account Management Module), and direct signal-based copy trading. Each has distinct implications for fee structure, fund manager liability, regulatory treatment, and follower capital segregation.

Most operators launch PAMM for structured fund management — where the manager controls a master account and follower capital is allocated proportionally — alongside signal-based copy for retail follower engagement. PAMM generates larger average follower deposits; signal-based copy generates higher trade volume and spread revenue. Running both is not more complex than running one if the infrastructure is designed for it.

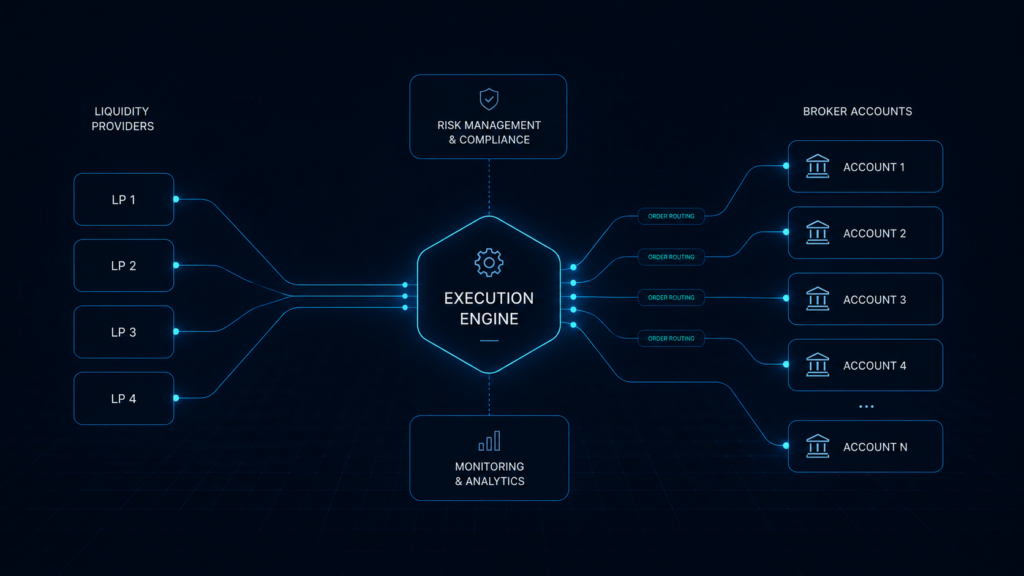

Step 2 — Integrate at the Execution Layer, Not Above It

The architecture decision that determines everything else: copy trading must integrate at the execution layer of the primary platform, not as an overlay. Practically, this means signal capture occurs at the trade confirmation event — not at order submission — and the replication engine has direct API access to the order management system.

Latency target: signal capture to follower order submission under 50 milliseconds in normal market conditions. Anything beyond 100 milliseconds begins to produce visible slippage on fast-moving signals. Anything beyond 200 milliseconds makes the product unreliable as a trading vehicle.

Step 3 — Configure the Risk Management Layer Before Going Live

Before a single follower account is activated, establish:

- Per-fund manager position limits: maximum aggregate follower exposure any single manager can generate

- Platform-level copy exposure limits: maximum total notional across all copy trades at any point

- Automated hedging triggers at the LP level when aggregate copy exposure breaches defined thresholds

- Risk dashboards that separate copy book exposure from direct client and proprietary positions — not combined reporting

The risk desk needs to see copy exposure as a distinct line item. Combining it with general book exposure obscures the concentration risk that copy trading can create.

Step 4 — Model the Fee Structure Before Recruiting Fund Managers

A sustainable three-tier fee model:

- Broker spread: Standard markup on all trades including copy trades. No exception for followers.

- Management fee: 0.5–2.0% AUM annually, collected by the fund manager from follower accounts. The broker retains a configurable share — typically 15–25%.

- Performance fee: 15–30% of profits, with a high-water mark that prevents fee collection on recovery from prior drawdowns. Broker retains a revenue share of the performance fee — commonly 10–25%.

Model the expected revenue from all three streams for your anticipated fund manager and follower base before launch. Fund managers will negotiate on fee terms; knowing your floor in advance prevents margin-eroding concessions.

Step 5 — Establish Fund Manager Qualification Standards

The product’s long-term performance depends almost entirely on the quality of fund managers listed on the platform. Define before launch:

- Minimum verified track record: 90 days of audited trading history is the operational standard

- Capital requirements for fund managers: managers should have meaningful skin-in-the-game capital in their master accounts — typically a minimum of $10,000–$25,000

- Performance thresholds for automatic delisting: maximum drawdown exceeding 25–30% is a standard trigger

- Risk-score calculation methodology that is visible to followers and updated in real time

Platform credibility is a function of the worst-performing manager visible on it. Delisting standards are not punitive — they are a product quality control.

Step 6 — Complete Compliance and Disclosure Review Before Launch

Copy trading occupies a regulatory gray zone in multiple jurisdictions. Depending on the structure, it may engage managed account provisions, collective investment scheme definitions, or discretionary management requirements under MiFID II, ASIC regulations, or other applicable frameworks.

The fund manager relationship structure — whether the broker is counterparty, platform facilitator, or something else — is the key regulatory variable. Document the structure clearly, obtain legal review under the primary license jurisdiction, and ensure all follower-facing disclosures are in place before the first account goes live.

Infrastructure for Operators Who Want This Built Correctly

SpencerLogic’s Invest Social platform provides native copy trading infrastructure — PAMM and signal-based copy both supported — integrated at the execution layer rather than layered via plugin. The Spencer Trader platform handles direct client trading alongside copy follower accounts within a unified execution environment, eliminating the latency gap that defines plugin-based architectures.

Risk controls for copy exposure operate through the AI Risk Management suite and the Risk Management Suite, with real-time aggregate copy book monitoring and configurable hedging triggers at the LP level. The Price Engine maintains sub-10-millisecond latency to liquidity providers through the Liquidity Aggregation layer, ensuring copy trade execution remains within the same envelope as direct client orders.

For operators adding copy trading to an existing deployment, SpencerLogic functions as an all-in-one white label brokerage solution — modular by design. Copy trading infrastructure integrates into an active SpencerLogic-powered brokerage without replacing components that are already in production.

Conclusion

Copy trading launches fail predictably at one of three points: execution latency creates visible slippage that erodes fund manager metrics, risk management gaps accumulate hidden directional exposure, or fee model misalignment produces a product that generates follower volume without generating brokerage margin.

The technical requirements to avoid each failure point are well understood. The gap between brokerages that profit from copy trading and those that treat it as an underperforming feature is almost always architectural — execution layer integration versus plugin overlay, native risk controls versus manual monitoring, pre-modelled fee structures versus retrofitted terms.

Operators who want to walk through what a properly integrated copy trading environment looks like in practice — latency specifications, risk control configuration, fee model design — can book a technical conversation with the SpencerLogic team. The conversation is structured around your existing stack, not a generic product overview.

FAQ

What is the operational difference between PAMM and signal-based copy trading for a brokerage operator?

PAMM pools follower capital under a fund manager who trades a single master account; profits and losses are allocated across follower accounts proportionally at the point of settlement. Signal-based copy trading replicates individual trades from the signal provider to follower accounts in real time, with followers maintaining separate accounts. PAMM typically generates larger average follower deposits and longer holding periods; signal-based copy generates higher per-account trade volume and spread revenue. Running both is standard for brokerages that want to serve both institutional-leaning fund managers and retail-oriented signal followers.

What latency is acceptable for copy trade execution?

Sub-50 milliseconds from signal capture to follower order submission is the operational benchmark for liquid market conditions. At 100 milliseconds, slippage on fast-moving signals begins to compress follower PnL in a manner that is visible in fund manager performance statistics within 60–90 days of launch. At 200+ milliseconds, the product becomes unreliable on any significant market event. The latency target must be a hard technical requirement, not a guideline.

How does copy trading affect the broker’s risk book?

Copy trading generates concentrated directional exposure when popular fund managers enter large positions. Without dedicated aggregate monitoring, this exposure accumulates alongside direct client and proprietary positions without appearing as a distinct risk line. Brokers need copy book exposure dashboards — separate from general book reporting — and pre-configured LP hedging triggers. The concentration risk is highest during high-volatility market events, which are also when manual monitoring is least reliable.

Does a brokerage need a separate regulatory approval to offer copy trading?

This depends on jurisdiction and structure. In the EU, copy trading arrangements may trigger MiFID II provisions around discretionary management or collective investment scheme definitions. In offshore jurisdictions, regulatory treatment varies significantly by license type and how the fund manager relationship is structured. Legal review under the specific primary license, before launch, is non-negotiable.

What fund manager metrics should be displayed to followers?

At minimum: maximum drawdown, Sharpe ratio or similar risk-adjusted return metric, win rate, average trade duration, number of active followers, and AUM. Brokers should also display a risk score — a composite metric that includes drawdown, volatility, and leverage usage — and a performance chart showing equity curve over the verified track record period. Transparency in manager metrics is directly correlated with follower conversion and retention.

How does copy trading change client acquisition economics?

Fund managers with established followings effectively bring their own client pipelines. A brokerage offering competitive performance fee terms on a reliable platform can acquire 50–200 follower accounts per top-performing fund manager with near-zero direct acquisition cost. For operations modelling blended CAC across the platform, copy trading is one of the few brokerage product structures where the operator benefits directly from network effects embedded in the product.

Can an MT4/MT5 brokerage add copy trading without rebuilding the platform?

Yes, but the architectural decision is consequential. Plugin-based approaches deploy faster but inherit the execution latency and risk visibility gaps described in this guide. Native execution-layer integration takes longer to configure but eliminates those limitations structurally. The correct choice depends on expected copy trading volume, the strategic weight of copy trading in the revenue model, and tolerance for visible slippage on fast market events.

To understand the technical architecture for your specific stack, book a demo with SpencerLogic.