Most brokers add copy trading first. It’s the lightest regulatory lift, the easiest client onboarding pitch, and the fastest path to incremental volume. But at some point, the traders on that platform start attracting real capital — clients who want to delegate entirely, not just mirror a signal. That’s when PAMM and MAMM stop being vendor brochure terms and start being architectural decisions with meaningful revenue and compliance implications.

The distinction matters because brokers routinely conflate them. Both involve a money manager trading on behalf of clients. Both generate volume the broker wouldn’t otherwise see. But they operate differently at the account structure level, they attract different types of managers, they carry different regulatory weight, and they require different back-office infrastructure. A broker that sets up PAMM expecting MAMM flexibility — or vice versa — will spend months unwinding the configuration.

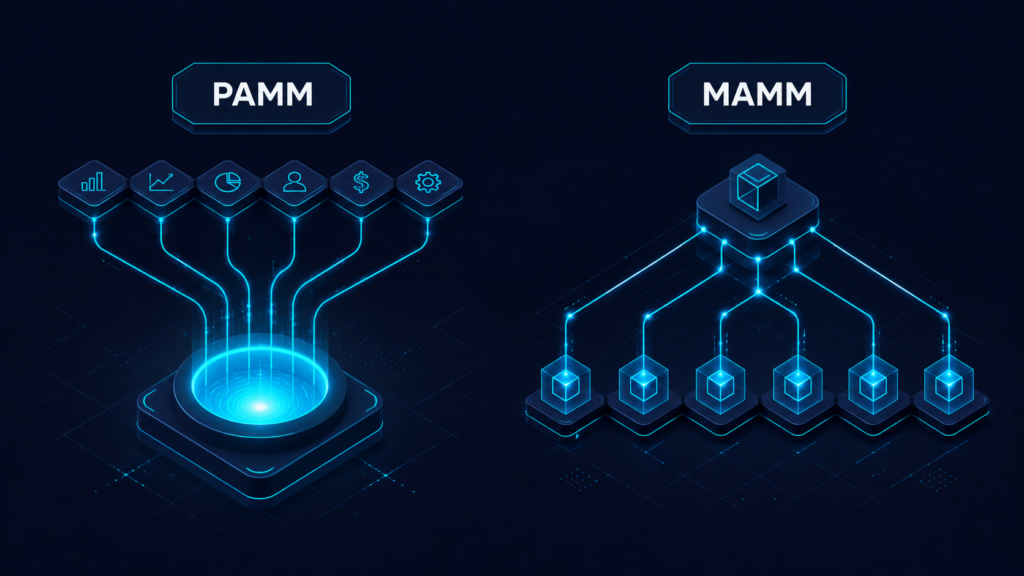

How PAMM Works: Pooled Capital, Proportional Settlement

PAMM — Percentage Allocation Money Management — pools client funds into a single trading account controlled by a fund manager. Each client’s share of that pool is recorded as a percentage of the total. When the manager closes trades, profits and losses are allocated back to each investor proportionally to their equity stake.

The manager never holds a custody relationship with client funds; they hold trading authority through a limited power of attorney arrangement. The broker is the custodian. Settlement — performance fee distribution, withdrawal processing, period-end reconciliation — runs through PAMM software that automates the allocation calculation. Without that software, the settlement math becomes operationally unmanageable at scale.

Key structural characteristics:

- Single master account; all client equity pooled

- Allocation by equity percentage at the time of trade close

- Manager compensated through performance fee, charged against gains

- Clients cannot intervene in individual trades while in pool

- Withdrawal windows typically scheduled (daily, weekly, monthly) rather than real-time

The pooled structure makes PAMM particularly strong in markets where investors are comfortable with a fund-style delegation model: the Middle East, Eastern Europe, and parts of Southeast Asia. It also makes performance reporting clean and auditable — one account, one track record, one set of statements. That audit trail is an asset when the manager is marketing to institutional-grade allocators.

The regulatory implication: pooling client funds, even under a limited power of attorney, attracts discretionary fund management regulation in most jurisdictions. Brokers operating under Vanuatu, SVG, or similar offshore frameworks typically have latitude to offer PAMM without additional licensing, but any ESMA or FCA-adjacent offering requires careful legal review of how the pooled structure is characterized.

How MAMM Works: Sub-Account Architecture, Manager Replication

MAMM — Multi-Account Money Management — takes a different structural approach. The manager trades from a master account. The platform replicates those trades across individual sub-accounts using allocation logic (lot-proportional or percentage-proportional, configurable per sub-account). Each client retains their own segregated account with their own balance, margin, and trade history.

The practical difference for the client: they can see exactly what’s in their account, withdraw on their own schedule (subject to open position constraints), and in some implementations adjust allocation parameters such as maximum lot size or drawdown limits. The manager is executing a strategy; the platform is doing the replication math in real-time.

Key structural characteristics:

- Separate sub-account per client; no pooling of funds

- Trades replicated from master account on execution, not settlement

- Lot allocation configurable per sub-account (flat lot, equity-proportional, leverage-adjusted)

- Clients retain individual account access and real-time visibility

- Withdrawals can run independently without disturbing manager positions

MAMM typically attracts higher-net-worth clients and fund managers who run more sophisticated strategies — discretionary traders, algorithmic managers, or multi-strategy operators who need per-client exposure control. The segregated account structure is also cleaner from a regulatory standpoint in many jurisdictions because funds are never pooled: each client maintains a direct relationship with the broker, and the manager’s authority is limited to trade execution.

The Revenue Comparison

Both models generate spread revenue on every trade. The dynamics differ in volume concentration.

Illustrative scenario — 10 money managers, 200 clients:

| PAMM | MAMM | |

|---|---|---|

| Trade execution | 10 manager accounts (one per fund) | 10 master + 200 sub-accounts |

| Volume per trade | Proportional to pooled AUM | Multiplied across sub-accounts |

| Withdrawal friction | Scheduled windows; lower churn | Real-time; higher activity |

| Fee complexity | Performance fee automation required | Per-sub margin and allocation management |

| Lot multiplication | Manager lots × 1 | Manager lots × n sub-accounts |

MAMM generates more raw volume per manager trade because each sub-account executes an allocated copy simultaneously. A manager placing a 10-lot order across 50 sub-accounts at proportional allocation produces 50 execution events at the sub-account level — with corresponding spread revenue on each. That volume uplift is why MAMM is often the higher-revenue structure for brokers with a populated managed account desk, even if AUM per manager is comparable.

The tradeoff is operational complexity. MAMM requires real-time replication infrastructure that can handle allocation logic across hundreds of sub-accounts without execution delay. Slippage between master trade and sub-account fill is the primary performance risk. Brokers relying on plugin-based replication rather than native allocation engines typically see meaningful slippage drag at scale, which shows up in manager performance statistics and eventually in client churn.

What Brokers Actually Decide

The choice between PAMM and MAMM isn’t binary in practice. Most serious managed account operations offer both, letting the market self-select. Signal providers who run high-frequency strategies with smaller per-trade risk tend toward MAMM. Managers running discretionary mid-frequency strategies with larger average positions and a preference for clean investor reporting tend toward PAMM.

The decision that does matter early: which to prioritize at launch.

Prioritize PAMM first if:

- Target market has appetite for fund-style delegation (Gulf, Eastern Europe, parts of Southeast Asia)

- Existing client base has traders with a demonstrable track record who can anchor a fund

- Regulatory framework allows pooled structures under existing license

Prioritize MAMM first if:

- Target client profile skews high-net-worth with preference for account segregation

- Introducing broker network has existing fund manager relationships who want client-level transparency

- Volume multiplication across sub-accounts is the primary revenue goal

Offer both from day one if:

- Launching a dedicated copy/managed trading product as a core feature (not an add-on)

- Platform infrastructure already supports real-time multi-account replication

- Manager acquisition strategy spans both retail signal providers and professional fund managers

Infrastructure Requirements Before You Go Live

The managed account desk is only as good as the allocation engine behind it. These are the components that need to be in place before client funds move:

1. Allocation engine — Handles the calculation of lot sizes or equity percentages per sub-account on PAMM settlement or MAMM execution. Must run without manual intervention and reconcile correctly on partial fills and margin events.

2. Performance fee computation — PAMM performance fees are typically charged at settlement periods (end of month, high-water mark reset). The software must track each client’s equity correctly across periods, handle deposits and withdrawals mid-period without distorting the fee calculation, and produce auditable statements.

3. Fraud detection against wash trading — Managed account infrastructure creates an incentive structure for wash trading between manager and investor accounts. The platform needs controls to detect cross-account manipulation — unusual correlation between manager and follower accounts, circular flows between related accounts, or performance fees generated through orchestrated position cycling.

4. Drawdown controls — Automatic pause mechanisms that halt manager execution when a configurable drawdown threshold is breached. This is a client protection feature, not just a risk management feature. In regulated markets, it may be a licensing requirement.

5. Reporting and statements — Clients in both PAMM and MAMM need period-end statements that show their equity contribution, the manager’s trading activity, performance fee deductions, and net return. Producing these manually is operationally unsustainable beyond a handful of accounts.

This is where platform architecture determines whether the managed account desk is a profitable product line or an operational liability. Brokers that build PAMM/MAMM on top of MT4/MT5 through third-party plugins inherit the limitations of those plugins — specifically, execution sequencing delays and limited allocation logic flexibility. Native allocation engines, integrated at the platform level, eliminate that constraint.

Positioning the Managed Account Desk as a Business

Beyond the infrastructure question, the more consequential decision is how to position the product.

A managed account desk run as an afterthought — a tab in the client portal with minimal onboarding support for managers — produces thin results. The model requires active work on both sides: attracting and vetting managers, providing performance leaderboards that give investor confidence, and building onboarding flows that convert qualified investors without creating compliance exposure.

Brokers that treat the managed account desk as a two-sided marketplace — with deliberate manager acquisition, transparent performance reporting, and investor onboarding infrastructure — see materially different outcomes. Managed account clients typically deposit larger initial amounts, show lower churn, and generate more volume per account than standard retail clients because they’re not making day-to-day trade decisions. The economics of the client relationship improve across every metric.

The infrastructure question and the business positioning question are related: a broker that takes the managed account desk seriously needs a platform that supports it end-to-end, rather than layering PAMM/MAMM functionality onto a stack that wasn’t designed for it. SpencerLogic’s Invest Social platform handles PAMM and MAMM natively, with allocation logic, performance fee automation, drawdown controls, and manager leaderboards integrated at the execution layer — not bolted on post-launch.

Brokers already running standard copy trading through Invest Social can activate managed account functionality without rebuilding their stack. For brokers evaluating a full infrastructure upgrade — trading platform, liquidity aggregation, bridging, risk management, and managed account capability — the all-in-one white label brokerage solution means the managed account desk is live from day one rather than a Phase 2 project.

Conclusion

PAMM and MAMM are not interchangeable. They serve different manager profiles, attract different client types, and have different operational requirements. Brokers who understand the mechanics make better launch decisions and build managed account desks that actually generate revenue. Those who conflate them end up with the wrong infrastructure for the client relationships they’re trying to attract.

The more important question isn’t PAMM or MAMM — it’s whether the platform behind the desk can support the allocation logic, fee computation, fraud controls, and reporting that make the product scalable beyond the first ten accounts. Start with the infrastructure question, then decide which product to lead with.

FAQ

What is the main difference between PAMM and MAMM?

PAMM pools all client funds into a single master account, with profits and losses distributed proportionally at settlement. MAMM keeps each client’s funds in a separate sub-account and replicates the manager’s trades across those accounts in real time. The key distinction is whether client funds are pooled (PAMM) or segregated (MAMM).

Which generates more volume for the broker — PAMM or MAMM?

MAMM typically generates more raw trading volume. Because each manager trade replicates across multiple individual sub-accounts simultaneously, the broker sees an execution event for each sub-account. A 10-lot manager order across 50 sub-accounts produces 50 allocated executions. PAMM generates volume at the pooled account level, which is typically lower.

Is PAMM regulated differently from MAMM?

In most jurisdictions, PAMM carries more regulatory scrutiny because it involves pooling client funds under a manager’s control — a structure that resembles discretionary fund management. MAMM, where client funds remain in individual segregated accounts, is generally treated as a managed account service with the broker as custodian. The specific regulatory treatment depends on the jurisdiction. Brokers should obtain legal advice before offering either product.

What infrastructure do I need to run a PAMM desk?

At minimum: a PAMM allocation engine that handles equity-proportional settlement, performance fee computation with high-water mark tracking, period-end client statements, and drawdown controls that pause manager execution at configurable thresholds. Fraud detection logic to identify wash trading is also necessary at any meaningful scale.

Can I offer PAMM and MAMM on MT4/MT5?

Both can be implemented on MT4/MT5 through third-party plugins, but plugin-based implementations carry execution sequencing limitations — specifically, latency between manager trade and sub-account allocation that produces slippage. Native allocation engines, built at the platform level rather than layered on top, eliminate that constraint. The choice matters more as the desk scales beyond 50–100 accounts.

How do I attract quality fund managers to a new PAMM/MAMM desk?

The primary acquisition channels are existing introducing broker relationships, trading communities with active signal providers, and direct outreach to independent fund managers who are currently using third-party platforms. Performance leaderboards with verified track records, transparent fee structures, and low minimum AUM thresholds for new managers accelerate early adoption. The desk needs at least three to five established managers before investor-facing marketing produces meaningful results.

What is a high-water mark and why does it matter for PAMM?

A high-water mark is the highest net asset value a PAMM account has reached before a performance fee is charged. Performance fees are only assessed on returns above the previous high-water mark — meaning the manager must recover any prior losses before earning further performance fees. This protects investors from paying performance fees on recovery from drawdowns and is considered standard practice in professionally managed PAMM products.